Eliminating ‘unfettered averaging’ one of the goals of new accounting standards…

The changes to Accounting Standard IFRS15 is just one of four new IFRS standards coming into force over the next few years as part of a move to enforce new global accounting rules aimed at transparency and “long-term financial stability of the global economy”.

The changes to Accounting Standard IFRS15 is just one of four new IFRS standards coming into force over the next few years as part of a move to enforce new global accounting rules aimed at transparency and “long-term financial stability of the global economy”.

Essentially, the new accounting standards will affect the way companies – especially the telecom, tech and utilities sectors – recognise revenue. Long story short, changes to the accounting and reporting process are hitting you from January 1, 2018.

We asked Trevor Paulauskas, Melbourne-based SAP principal consultant for Financial Management at Oxygen (part of DXC Technology), to explain.

“Essentially the taxman wants to recognise your revenue upfront as related to what you’re actually selling,” he said.

“This is mainly aimed at telecommunications and hi-tech equipment sellers. Take a cellphone for example. Often that item will be sold alongside an ongoing service. The charges will include the cost of the item plus a charge per month for maintaining a service.”

The new rules, said Paulaskas, basically say that if the telephone costs $500 and the rental costs $700, out of that $1200 total, the handset cost needs to be recognised upfront as a revenue item.

“In the first month where you’re doing your accounting, you need to recognise that handset as a sale in the first month and then the remaining $700 for the rental can be split evenly across the following 12 months.”

Sounds simple enough, but by all accounts it’s going to be a royal pain in the ass come tax time.

“Really, you need to start to engaging with your auditors and business process owners to see, firstly, whether you should be considering this RRAR (Revenue Recognition Accounting and Reporting), and to look at how these changes are likely to impact you. Don’t underestimate the degree of complexity and effort and time that is required to get things like this up and running,” Paulauskas said.

“People need to act sooner rather than later. Don’t leave this until the last minute, because it’s not a last minute sort of project.”

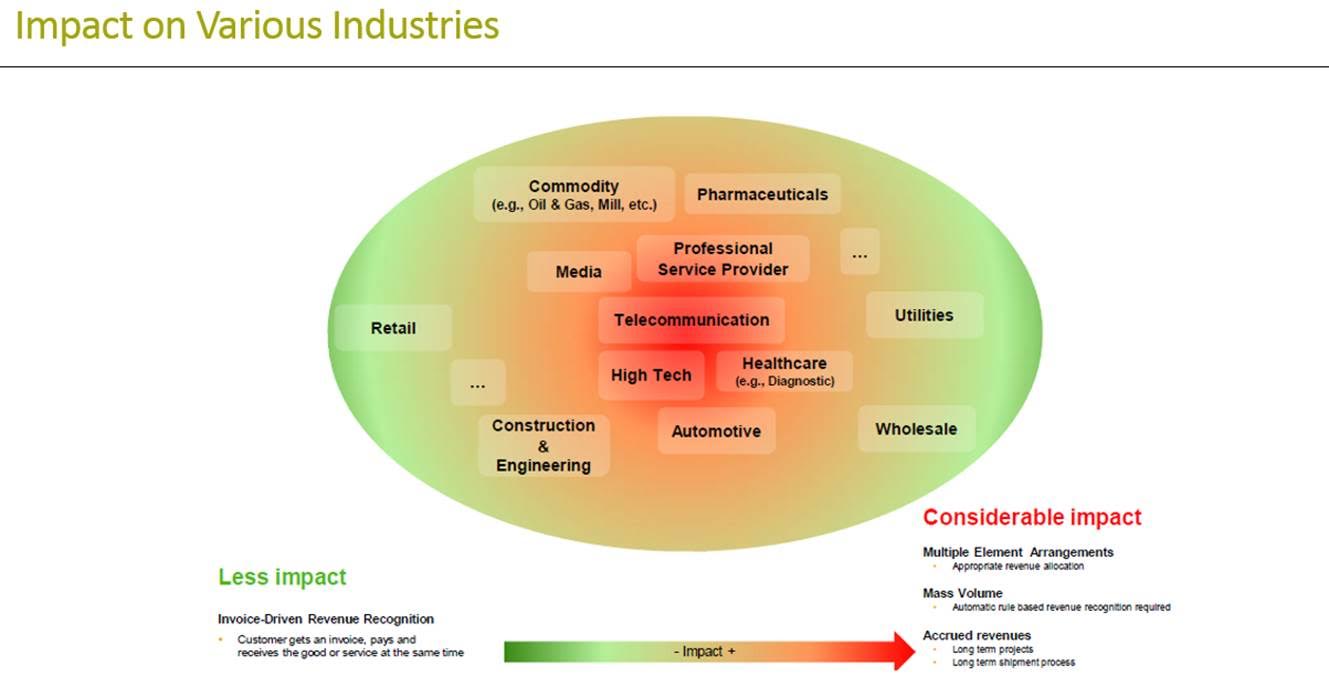

SAP has created a heat map (of sorts) to indicate the industries that are primarily affected by the new standards:

Source: SAP

So just what is behind the taxman’s latest decree?

Hans Hoogervorst, chairman of the International Accounting Standards Board (IASB), addressed just that question in plain terms at the annual IFRS Foundation Conference in Amsterdam at the end of last month, saying that it’s all in the interest of improving performance reporting across the board.

Many businesses regularly go through lean years of meagre profits and, when it comes to reporting, those businesses hope to make up for this during the business’s moments of upswing, Hoogervorst said.

Fair enough, but the problem, said Hoogervast, is that that makes it very difficult for investors to properly analyse the earnings trends of some companies.

“Earnings trends are often an early warning system of problems to come,” he said.

“If we want accounting to perform its function as the proverbial canary in the coal mine, it is important to avoid excessive averaging, even in a business where averaging of risks is an essential part of the business model.”

The new rules essentially ban unfettered averaging which can lead to accelerated or delayed earnings recognition. That makes it harder for investors to understand real earnings trends.

“Our primary goal is to develop IFRS standards that bring transparency, accountability and efficiency to financial markets around the world,” Hoogervast added.

“Proper accounting shines light on risks that might otherwise go unnoticed – both by companies themselves and by investors.”

Join Oxygen on 25 July for a Webinar: New revenue recognition rules IFRS15 to learn more.